Artificial intelligence (AI) is a powerful tool that financial institutions (FIs) can use to proactively enhance every aspect of the customer credit lifecycle. Download How to put AI in your FI business plan, a report from PYMNTS.com and Brighterion, for a detailed blueprint on how your FI can leverage AI in 2021.

Even before the pandemic upended literally everything early in 2020, American consumer household debt was at a 12-year high and FIs were mindful of the heightened need to monitor credit risk. The onset of the pandemic highlighted how FIs could use AI to pivot and assess new situations and new data in real-time with nuanced tools that deliver personalized services for their customers while also boosting their bottom lines. And given that rapid change and volatility are a constant today, not just in times of crisis, the ability to be nimble and accurate when assessing credit risk is essential. The power of AI to optimize each touchpoint of the customer credit lifecycle, from application scoring to delinquency risk to collections, cannot be underestimated by FIs who want to leverage AI to enhance their consumer credit operations.

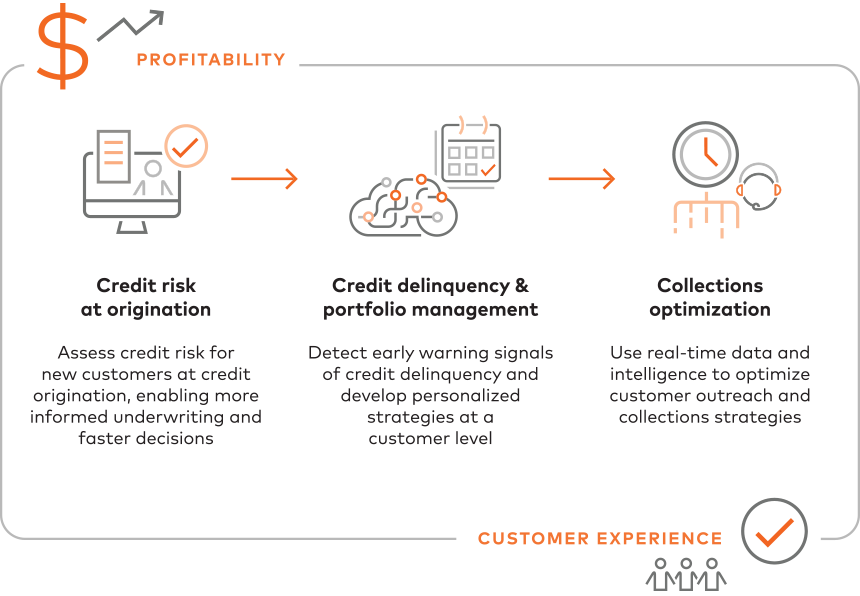

Credit application and origination scoring

Using AI to assess creditworthiness for customers allows for more data-driven decision making and an improved customer experience. Rather than relying on traditional data such as bank records and payment histories to determine application scoring, AI-driven credit scoring models can assess a consumer’s creditworthiness by analyzing “alternative data,” including their transaction histories, their usage of other products, and additional data feeds. This allows FIs to more accurately assess credit risk for new customers at credit origination, which can have a profound impact on consumers’ access to credit without increasing the risk to an FI’s credit portfolio.

Managing credit delinquency risk

Traditionally, managing credit delinquency risk has been a reactive process, with loan managers working with consumers to bring them back up to speed after they’ve become delinquent. With AI, it can become a proactive process as AI tools can analyze an enormous breadth of data to predict potential delinquency up to a year before it happens. The loan manager can then develop personalized strategies for preventing delinquency at a customer level, saving the FI time and money, and protecting the consumer’s creditworthiness.

Collections optimization

Managing collections by retroactively going after borrowers who have missed payments has negative consequences for both FIs who may lose money and the customer whose credit score may be affected. Instead of trying to collect money after the fact, why not support customers by helping them avoid missing payments in the first place? AI uses real-time data and intelligence to optimize customer outreach and collections strategies that make it easier for customers to make their payments on time. These optimization strategies increase consumer satisfaction and reduce the overall risk to an FI’s credit portfolio.

32%

Credit loss reduction

Using AI to manage the customer credit lifecycle has powerful benefits. Not only does it drive higher revenues for FIs by reducing credit losses and collections costs, but its predictive capabilities also allow FIs to offer the digital-first banking options that consumers have come to expect and value. In fact, 63.6 percent of FIs using AI say their customers’ satisfaction has increased, and 23.7 percent say their AI systems reduced the overall risk of their portfolios. More specifically, some of the largest global lending institutions have reduced credit losses by up to 32% when using Brighterion AI. FIs can leverage smarter AI-based banking tools and systems to offer banking and financial services that customers can access via their preferred platforms – whether that’s in person or online, or a combination of both – improving the overall banking experience for customers and customer retention for FIs.

Despite these benefits, it can be unclear to FIs exactly what AI is and how it can enhance their specific credit risk operations. AI is not restricted to data mining, business rules management systems and case-based reasoning, it goes far beyond that. And the ROI can seem intangible until you put AI tools and systems into place, so it’s important to truly understand what AI is and how it can support your FI before you begin the implementation process. Building up in-house AI expertise is expensive and time-consuming, while outsourcing AI to a third party expert such as Brighterion saves cost and time and allows you to see the advantages AI offers more immediately. The following tips for improving your AI IQ and removing the guesswork from AI adoption will help you better understand AI’s benefits.

Checklist: How to improve your AI IQ

Doing your AI legwork will help decision-makers determine the benefits of AI for their organizations. Here’s how:

- Do your research into how peer institutions are using AI, the latest news on AI in banking, and the different AI products available

- Enlist your in-house risk team, including loan officers, account managers, software engineers, legal professionals, and AP specialists, to help you assess how AI can improve your consumer credit operations

- Choose a third-party AI provider who specializes in AI solutions for FIs, such as Brighterion, rather than trying to build AI expertise in house

- Test AI use cases by rolling out AI applications one at a time to test and track their ROI before expanding how you’re using AI internally

Checklist: How to remove the guesswork from AI adoption

Before you implement AI, it’s important to understand the true ROI it will bring to your FI. The following six steps will help FIs clarify how to leverage AI and the resources needed for AI implementation:

- Identify use cases

- Define the specific operations that can be enhanced with AI

- Determine what data is available to support those AI operations

- Detail and prioritize potential use cases

- Reach out to third-party providers like Brighterion

- Enlist third-party experts who can seamlessly feed your historical data into an AI system

- Third-party providers can then use that data to create FI-specific AI models

- Use case overview

- Your third-party provider can help produce data outputs that demonstrate the potential benefits of an AI system specifically for your FI. In Brighterion’s case it only takes 6-8 weeks from data extraction to results

- Compare legacy system performance to AI performance

- The outputs from step three can be used to illustrate how AI can improve specific operations compared to legacy systems

- Provide contrast

- Comparing and contrasting statistics will help quantify the benefits of adopting AI technology

- Deployment footprint

- The final step for FIs and their third party providers is to comprehensively assess how much funding, capital, and coordination is needed to implement a custom model for the FI. This data is necessary for determining if implementing AI would help meet their business objectives

Going into 2021, it’s imperative that FIs have a proactive plan to leverage AI to monitor credit risk and manage delinquency throughout the rest of the pandemic and beyond. Download our in-depth roadmap for FIs who want to use AI to optimize their consumer credit operations, How to put AI in your 2021 FI business plan. The report, a collaboration between Brighterion and PYMNTS.com, goes into more detail on how AI can help manage your credit portfolios, improve your operational efficiency and the steps you can take to ensure you are maximizing the return on investment from AI innovations.